No, I really don't follow your logic at all - PSU is the biggest MARKET DRAW in all of the East Coast markets that you keep talking about. If you couple PSU with any, or all, of their traditional rivals in their HOME REGION the Northeast & Middle Atlantic, PSU would deliver these same cable revenues to the ACC if they were in that conference (especially if ND became a full-time member in the North Division along with PSU, BC, sorryexcuse, ASWP, butgers, MD, etc....). The b1g turd conference has ZERO to do with generating these cable revenues in the Northeast and Middle Atlantic and PSU has everything to do with it.

Sorry, but you're introducing an apples and oranges argument. Let's recap what has happened. (Note: Any updates or modifications are welcome)

A) Penn State has a huge following, of course.

B) Penn State's revenue contributions in the 11 team market area and nationally, had already been factored in to Big Ten revenue, for decades.

C) The issue is the marginal contribution from adding Rutg & MD.

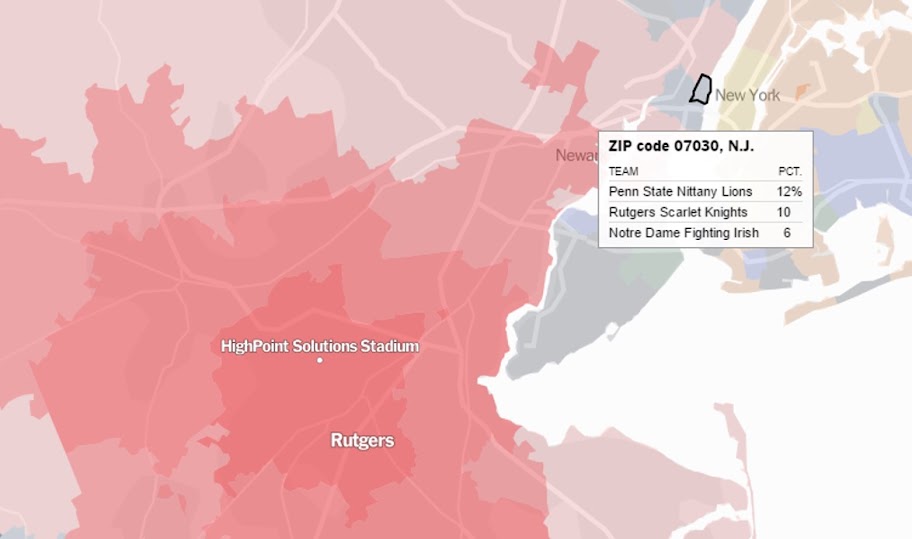

D) PSU and the 11 Team Big Ten had not gotten the higher revenue BTN cable deals in NYC, DC and Baltimore. IIRC - There was revenue from contracts with Disney/ESPN and the lower remote location BTN cable revenue, but not the higher levels of monthly cable subscribers' revenue, that is more likely with local area teams.

E) Reports show that beyond PSU's fan support in NYC, other BT teams also had quantifiable levels of fans. Those included teams like Mich, tOSU, Wisconsin in general, plus Indiana and MICH ST for BB, etc. Yet, the combined draw of the Big Eleven, including PSU, didn't net any of these new higher revenue BTN contracts with NYC, DC and Balt area cable suppliers. That's just the way it was. That left a lot more money on the table, that the old Eleven weren't enjoying.

F) IIRC - The combined package of the Big Eleven, plus NEB, Rutg and MD was the first time the BT was able to secure the higher subscription payments for the BTN via new cable deals in those big markets of NYC, DC and Balt.

G) The new combined 14 team package will likely be worth considerably more, when the 2017 contract gets negotiated with Disney/ESPN or any other Sports network that wants some of our combined BT programming. As a co-owner in the BTN, FOXSports might be a player, for example.

G) The reality is the Big Ten for PSU.

Contracts focus on with can be delivered and not with fantasies that can't be delivered. As such, I leave you to whatever speculation you want to have, regarding the ACC and some imaginary group of Eastern teams.

Have at it Bushwood CC. No harm in some friendly "What if" speculations. They can be fun exercises too and can make for some interesting reading.

Enjoy...